Rising Fuel Costs and the Shift to Energy Resilience

.png)

The recent escalation in conflict in Iran has sent shockwaves through global commodity markets. For many businesses, the reality is stark: energy costs have effectively doubled, creating an incredibly difficult environment for maintaining operations and profitability.

Diesel prices in parts of Australia rose by more than 80% in a matter of weeks. For energy-intensive industries reliant on diesel or gas-fired generation, this represents a sharp increase in operating costs and fuel price exposure, an uncomfortable echo of 2021.

For industrial site owners, it immediately begs a key question: how do we move beyond this vulnerability and transition to a world of energy resilience? And does this shift strengthen the case for investing in renewables and energy independence?

Modeling a Hybrid Industrial Energy System

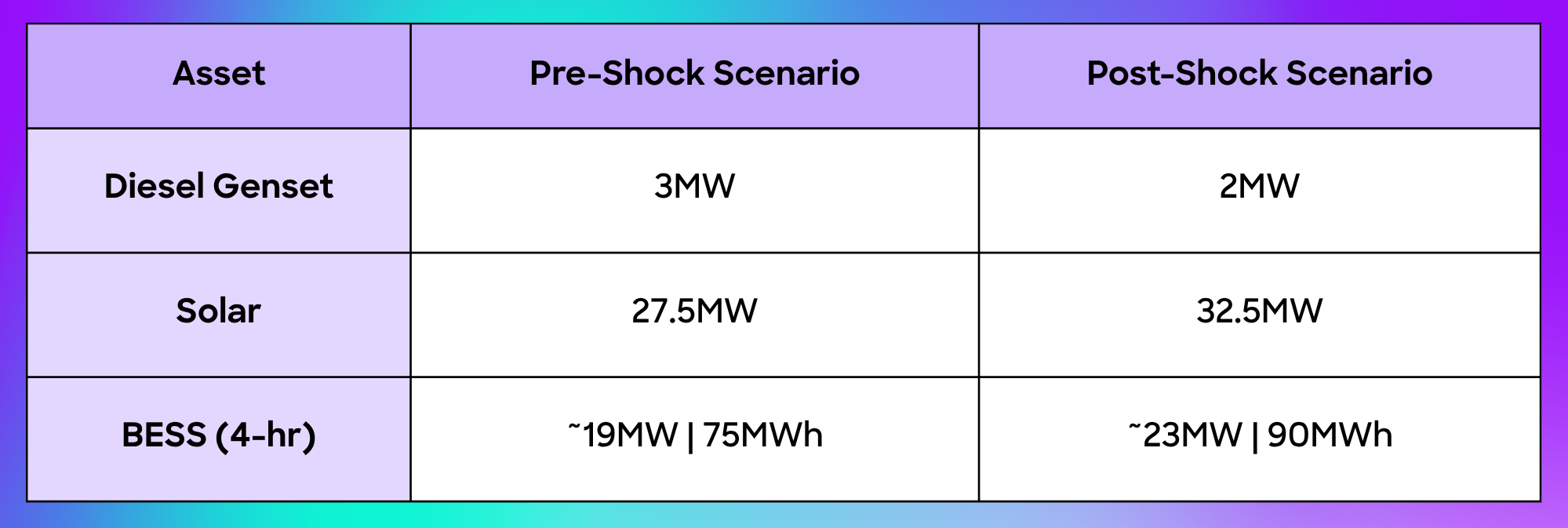

To explore this, I modeled a 10MW industrial site in New South Wales, Australia with a 5MW grid connection, requiring on-site generation to meet its full demand. The system includes a hybrid mix of solar, diesel generation, and battery storage, with asset sizing optimized under two distinct diesel fuel price scenarios:

- Pre-shock: $1.60 / L

- Post-shock (current conditions): $3.00 / L

Key assumptions include CSIRO GenCost capex, a 4-hour Battery Energy Storage System (BESS), a 20-year model, and a cost stack covering retail, network, and environmental charges. While fuel prices are unlikely to remain elevated for the entire modeling period, this analysis provides insight into how price shocks can influence long-term investment decisions and fundamentally change asset dispatch.

How Optimal Asset Sizing Changes

After running a simulation, the optimal asset sizing for pre-shock and post-shock fuel price scenarios is shown below:

Notice that diesel capacity decreases by 1MW. This highlights the continued need for thermal generation to maintain reliability during low-renewable periods. Due to the constrained grid connection and near 24/7 demand, both scenarios favor significantly oversizing solar and storage, which is more cost-effective than adding additional generator capacity.

In the post-shock scenario, solar and battery capacities increase by roughly 9% and 21% respectively, reflecting the reduced competitiveness of diesel generation at higher fuel prices.

Economic vs. Reliability Dispatch: Shifting Strategies

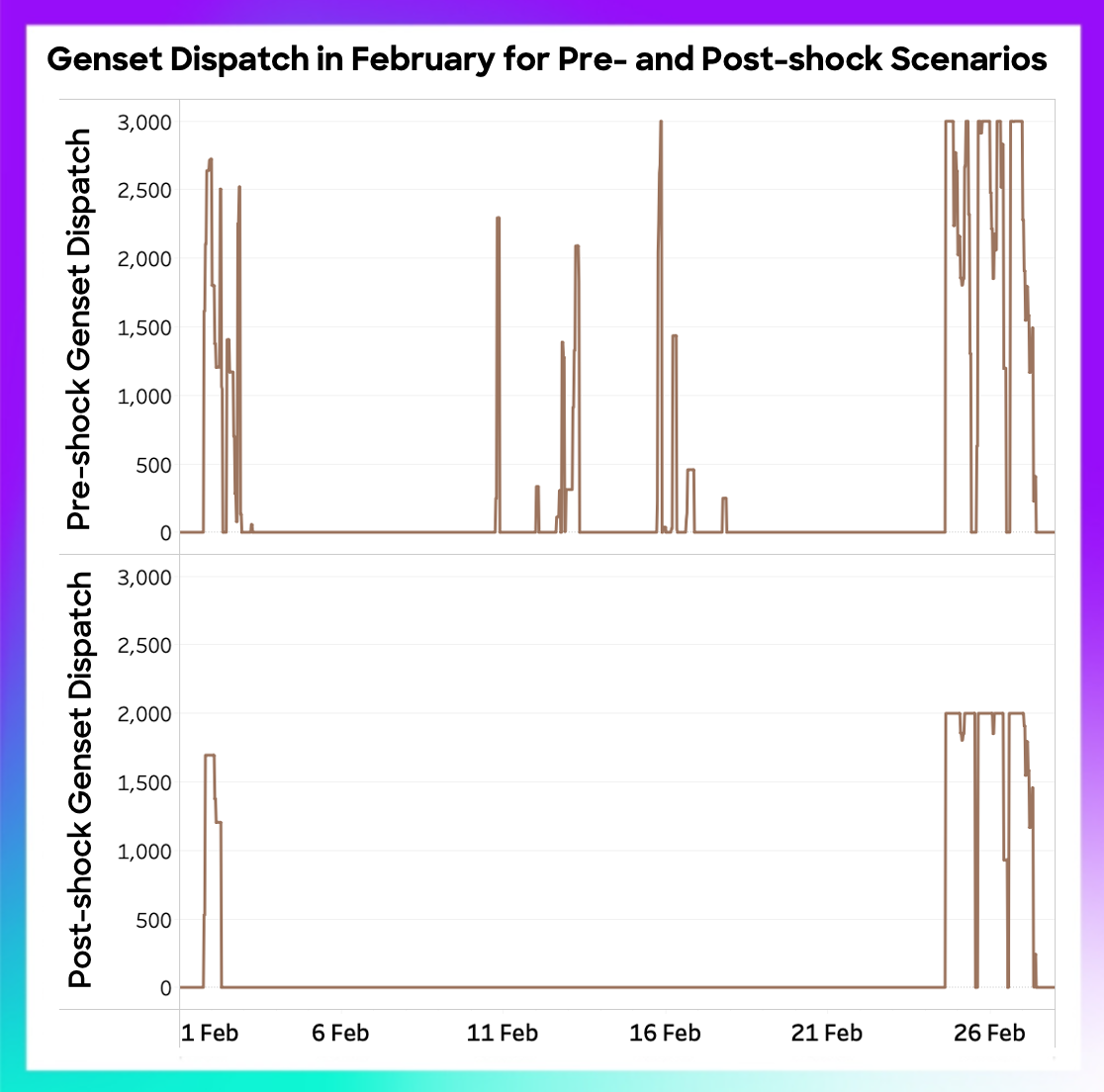

To what extent do increased fuel costs shift dispatch, and what can we learn? This shift is best understood by separating generator dispatch into two categories:

- Economic dispatch: Avoiding peak network and retail charges.

- Reliability dispatch: Avoiding unserved load.

In the pre-shock scenario, much of the generator dispatch aligns with network peak demand charge intervals. During these periods, the cost of diesel fuel is lower than the cost of incurring peak demand charges, driving economic dispatch. The remaining dispatch is driven by reliability, where on-site generation and battery state of charge cannot meet the load, and it is more cost-effective to burn fuel than to invest in additional solar and storage to eliminate unserved load.

In the post-shock scenario, these categories diverge. Reliability-driven dispatch remains, with thermal generation dispatching maximum capacity multiple times to cover unserved load. However, economic dispatch disappears entirely, as higher fuel costs outweigh the savings from avoiding peak charges. Instead, the system relies on the increased solar and battery capacity to meet demand during these periods, allowing peak intervals to be served without dispatching the generator.

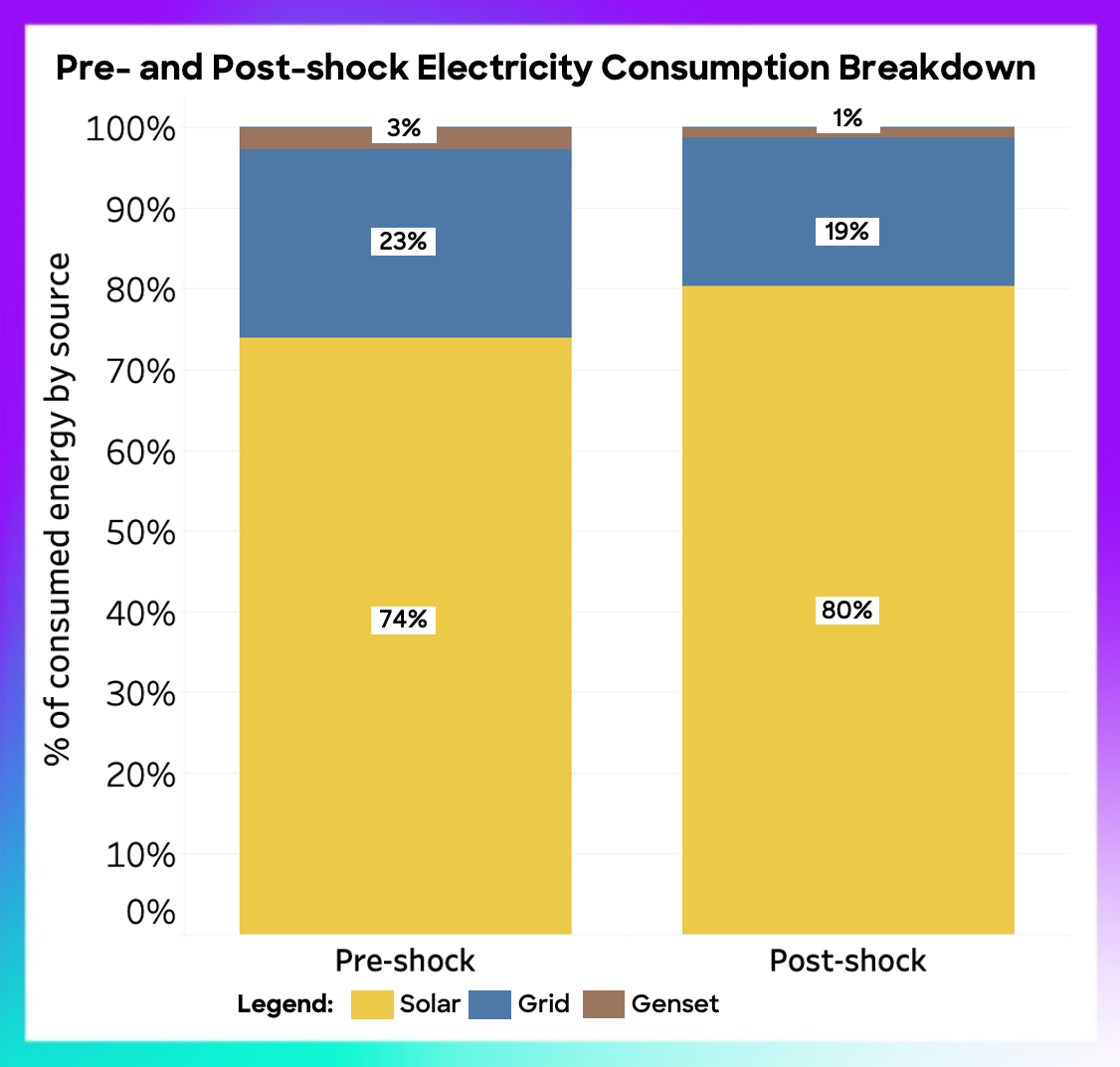

The Impact on Total Energy Consumption

This shift strategy is reflected in overall energy consumption. Solar contribution, including solar stored by the BESS for later use, increases by 6%, while grid reliance decreases by 4%. Meanwhile, the generator's contribution falls from 3% to just 1%.

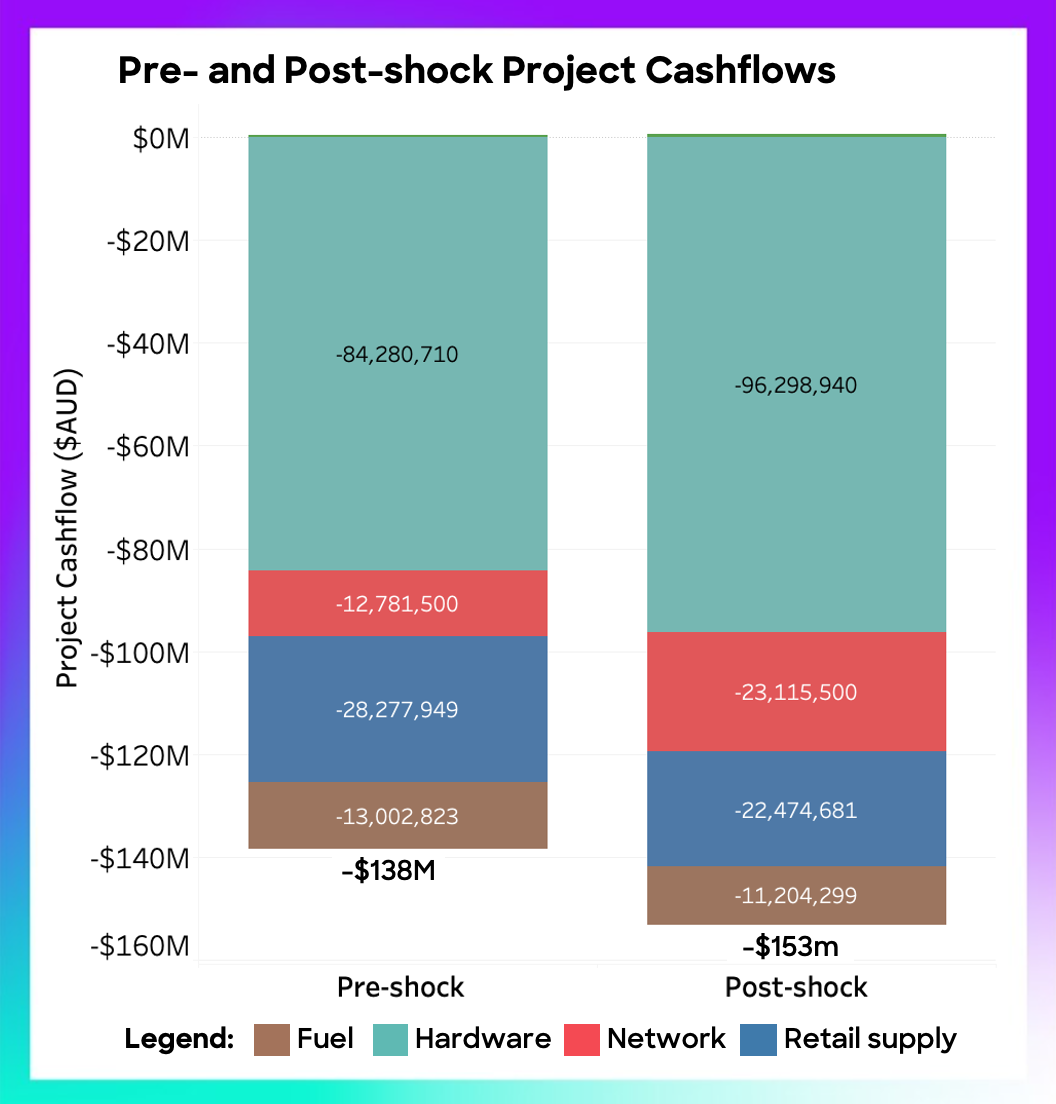

Naturally, this difference in energy consumption is reflected in the resulting project cash flows.

Does Energy Independence Outweigh Higher Upfront Costs?

Over the course of the 20 years, the post-shock asset configuration is around $15 million more expensive. The savings in fuel and retail supply do not outweigh the additional $12 million in hardware and $10 million in network costs.

What is perhaps most interesting is that, despite importing less electricity from the grid (reflected in a $6 million reduction in retail costs), network costs are actually $10 million higher. This suggests that cost outcomes are being driven less by total energy consumption and more by how and when the site interacts with the grid, particularly its exposure to peak demand charges.

In the post-shock scenario, even with increased solar and battery capacity, battery state of charge remains insufficient to effectively reduce peak demand all the time. The optimal asset sizing further indicates that additional solar and BESS capacity is not economically justified, as the incremental investment exceeds the potential reduction in network costs. At the same time, higher fuel prices constrain economic dispatch, with the cost of running thermal generation exceeding the savings that could be achieved through reduced demand charges.

What Limits the Value of Energy Independence?

Rather than simply increasing costs, the post-shock scenario demonstrates how fuel price shocks fundamentally change system behavior. As fuel prices rise, thermal generation transitions from an economically dispatched asset used to manage peak demand, to a reliability-only asset reserved strictly for avoiding unserved load.

This shift places greater reliance on solar and storage, but also exposes a key limitation. Even with increased capacity, battery state of charge is not consistently available during peak demand intervals. As a result, the system remains exposed to network demand charges, highlighting that cost outcomes are driven less by total energy consumption and more by the exact timing of grid interaction.

While increased investment in solar and storage reduces fuel exposure and improves energy independence, it does not fully mitigate peak-driven network costs. However, this dynamic may evolve as long-duration storage becomes more cost-competitive. With falling capex, longer-duration batteries have the potential to sustain discharge across extended peak periods, improving the ability to manage demand charges without relying on thermal generation.

Fuel price shocks may be temporary, but they reveal an important structural shift. As the economic role of thermal generation diminishes, system value increasingly depends on the ability of storage to deliver energy at the right time, not just in sufficient quantity.

Reach out to the Gridcog team if you're interested in modelling your energy projects.