Australia or Europe, who is best placed to succeed in the energy transition?

Australia or Europe, who is best placed to succeed in the energy transition? Since we at Gridcog work across both regions, I sometimes get asked this question.

Here are my brief thoughts.

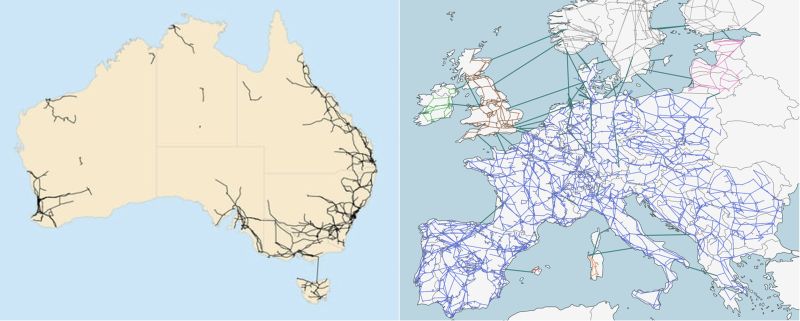

European countries have highly integrated power markets and cross-border interconnection, with the potential for much more, allowing diverse resource sharing across the continent: nuclear, hydro, wind, and solar.

Australia's stringy and sparse East-coast and West-coast transmission systems are isolated with very limited potential for international interconnection.In Australia's favour is more consistent renewable resources year-round, while Europe faces seasonal variability with low winter solar output and extended renewable droughts, compounding Europe's greater need for low-carbon heating in winter.Australia leads in distributed PV penetration, exceeding even Germany and the Netherlands.

This has turned Australia into an innovation leader with solutions like dynamic operating envelopes and virtual power plants. But Europe significantly leads Australia in the adoption of electric vehicles.Europe has deep, liquid day-ahead energy markets enabling independent power trading and marketing at scale. In Australia, it's tough to be a large supplier without significant physical generation assets, entrenching the existing 'gentailers', and limiting competition.

But, Australia does have more efficient system operations with locational pricing, 5-minute settlement, and co-optimised central dispatch providing clearer investment signals and ensuring resources are dispatched optimally to meet the systems needs.

European countries are more progressed phasing out coal due to stronger political support for decarbonisation, and the benefits of interconnected markets.

Australia has historically had higher coal dependence and is struggling to build replacement generation quickly enough, creating system risks due to a continuing dependence on an aging coal generation fleet.

Gas imports and seasonal gas storage is crucial for European industry and meeting winter demand. Europe has been busy since the Ukraine invasion to develop new gas import sources and is pursuing strategies to reduce future gas dependence through hydrogen (a very challenging proposition).Australia, while a major gas exporter, sadly linked its domestic gas market to international markets, exposing domestic users to very high prices, with big implications for manufacturing and power prices.

With Australia’s superior renewable resources, gas probably only has future as a peaking/balancing resource (albeit for decades more to come).

The implications? Both regions have viable pathways leveraging different advantages.Australia needs more internal interconnection and more power generation to enable coal retirement, while Europe must continue market integration and interconnection and find solutions to replace natural gas: renewable overbuild, hydrogen, seasonal storage, more nuclear, or all of the above?