Understanding P510: What it is, how it differs from P415, and what it means for asset owners

P510 is a proposed GB code modification that builds on P415 - and could significantly change how behind-the-meter flexibility is valued and settled across GB energy markets.

A growing number of flex assets and Virtual Trading Parties (VTPs) have been participating under P415 in recent months. As traded volumes have increased, some of the limitations of the current mutualised compensation structure have become more apparent. P510 proposes to address them.

Watch our full video on this topic, or keep reading below:

What is P510?

P510 proposes a shift from the mutualised compensation structure introduced under P415 to a bilateral arrangement between suppliers and VTPs. The aim is to enable bidirectional flexibility - properly accounting for both upward and downward deviations in settlement, and ensuring load shifting is exposed to real wholesale market signals.

What are the limitations of P415 that P510 addresses?

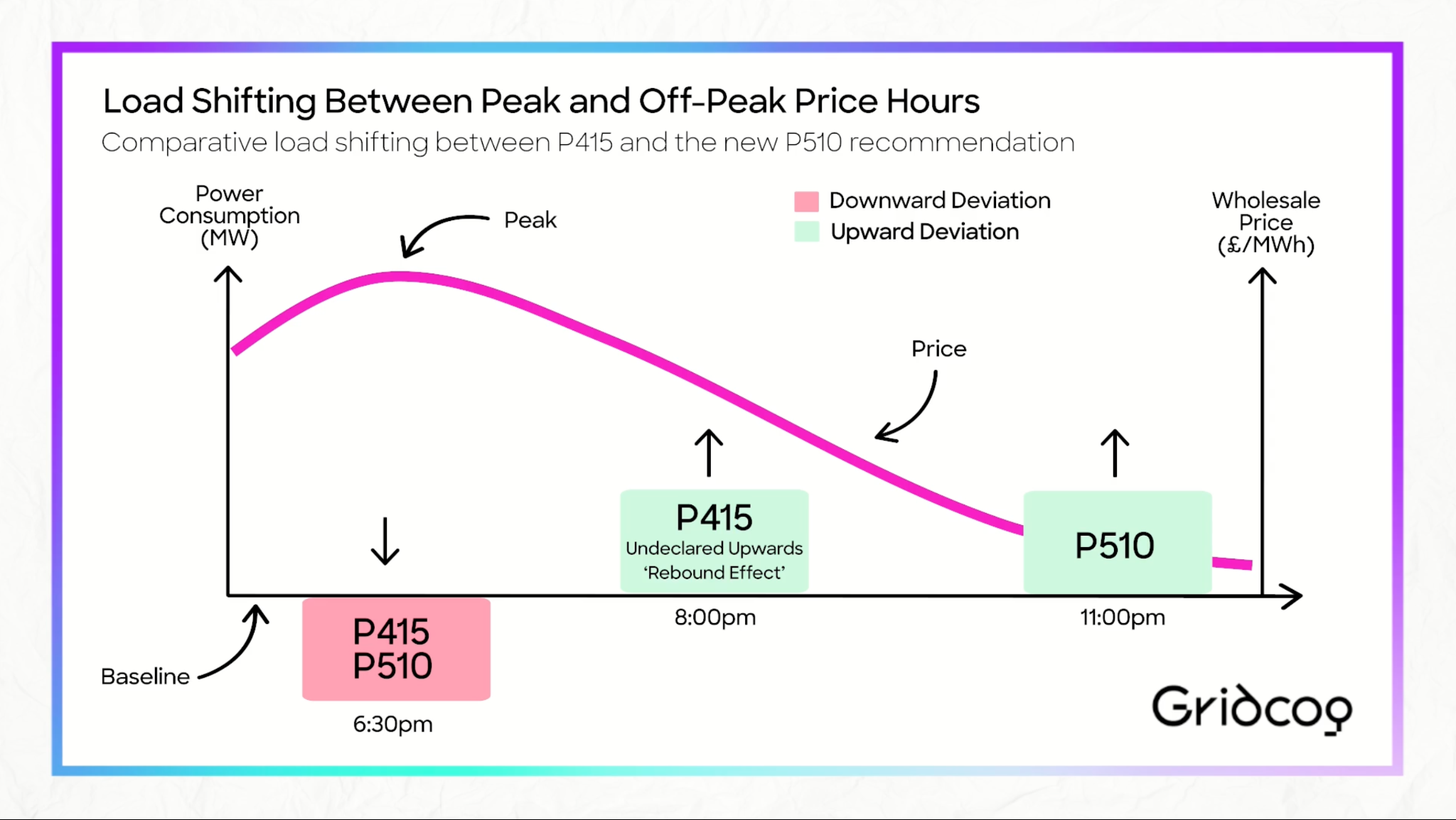

Under P415, VTPs are incentivised to reduce demand and monetise those volumes in the wholesale market. This leaves suppliers in a long position, with compensation drawn from a mutualisation pot.

However, VTPs are not compensated - and therefore not incentivised - to declare upward deviation actions where demand is turned up. This is a direct consequence of the current mechanism: upward deviations would require suppliers to pay into the pot, but that value never flows through to the customer or VTP.

.jpg)

There's also the rebound effect - where demand reduction is simply consumed later in a potentially unoptimised manner - which can increase overall imbalance costs.

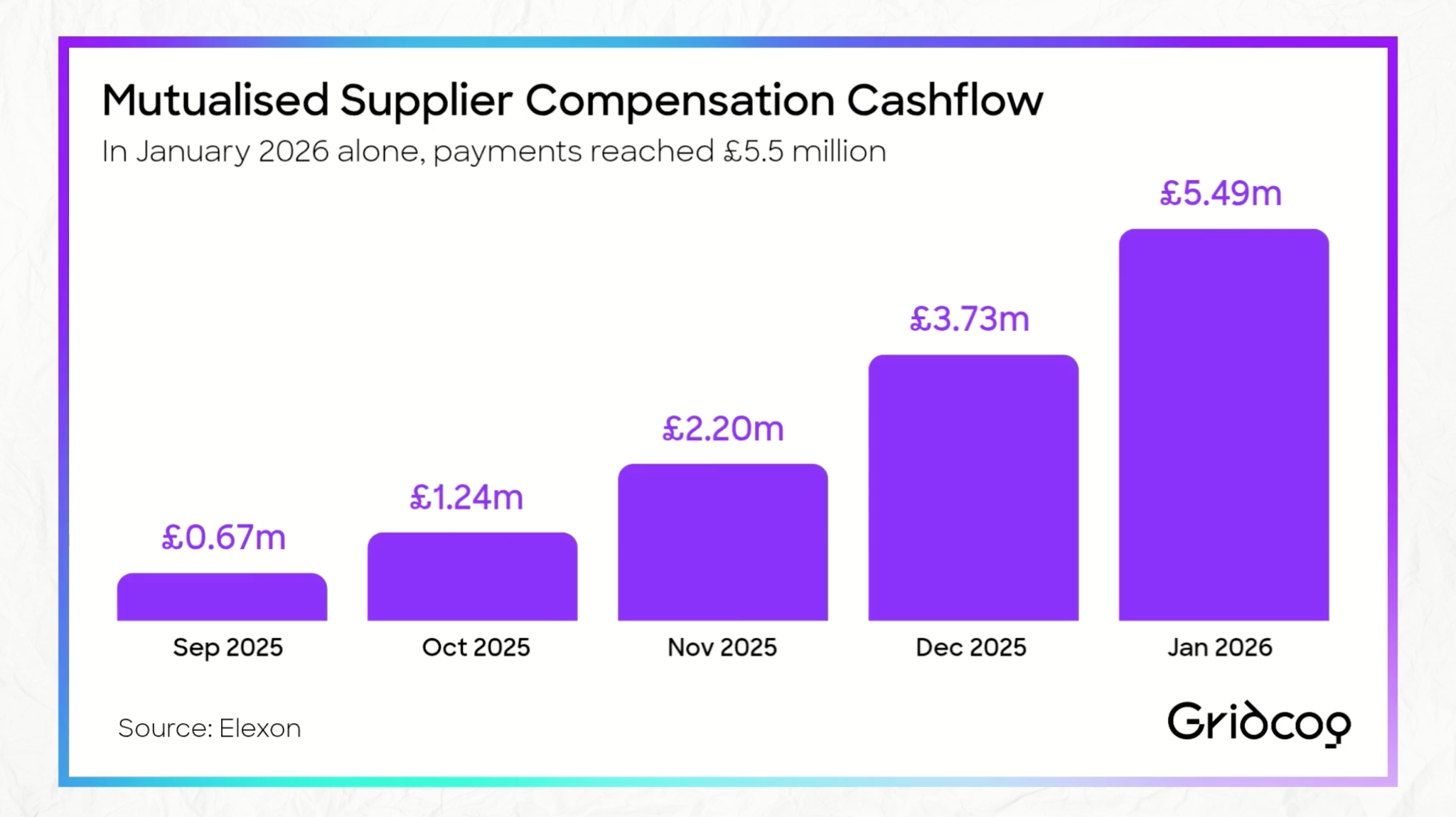

As traded volumes grow, so too does the size of the mutualisation pot. In January 2026 alone, payments reached £5.5 million.

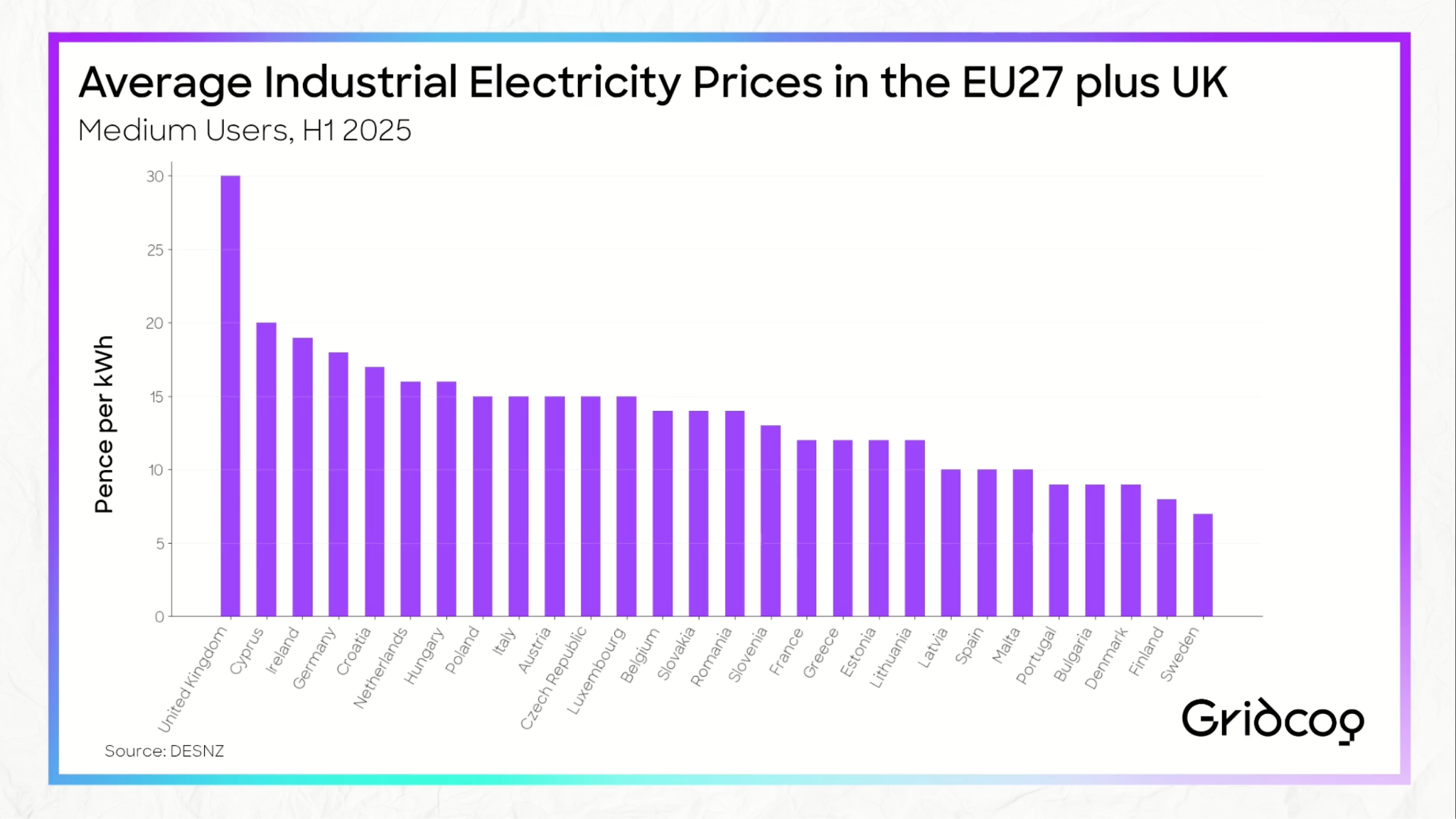

Over time, these costs are likely to be passed through to consumers, with those less able to flex effectively subsidising those who can. At a time when the UK already faces some of the highest electricity prices globally, this risks undermining consumer support for flexibility.

This problem is compounded by the growing need to absorb renewable generation: wind curtailment costs have already exceeded £600 million for consumers in 2026, and there were 149 hours of negative day prices in 2025.

How does P510 work?

P510 introduces a bilateral compensation structure between the VTP and the supplier, with both sides of the energy transaction exposed to wholesale market signals. Compensation flows at Ofgem's wholesale cap rate, producing a fairer, market-based value for load shifting - without adding wider system costs.

This also avoids the rebound effect by ensuring both the upward and downward sides of a load-shifting action are properly accounted for in settlement.

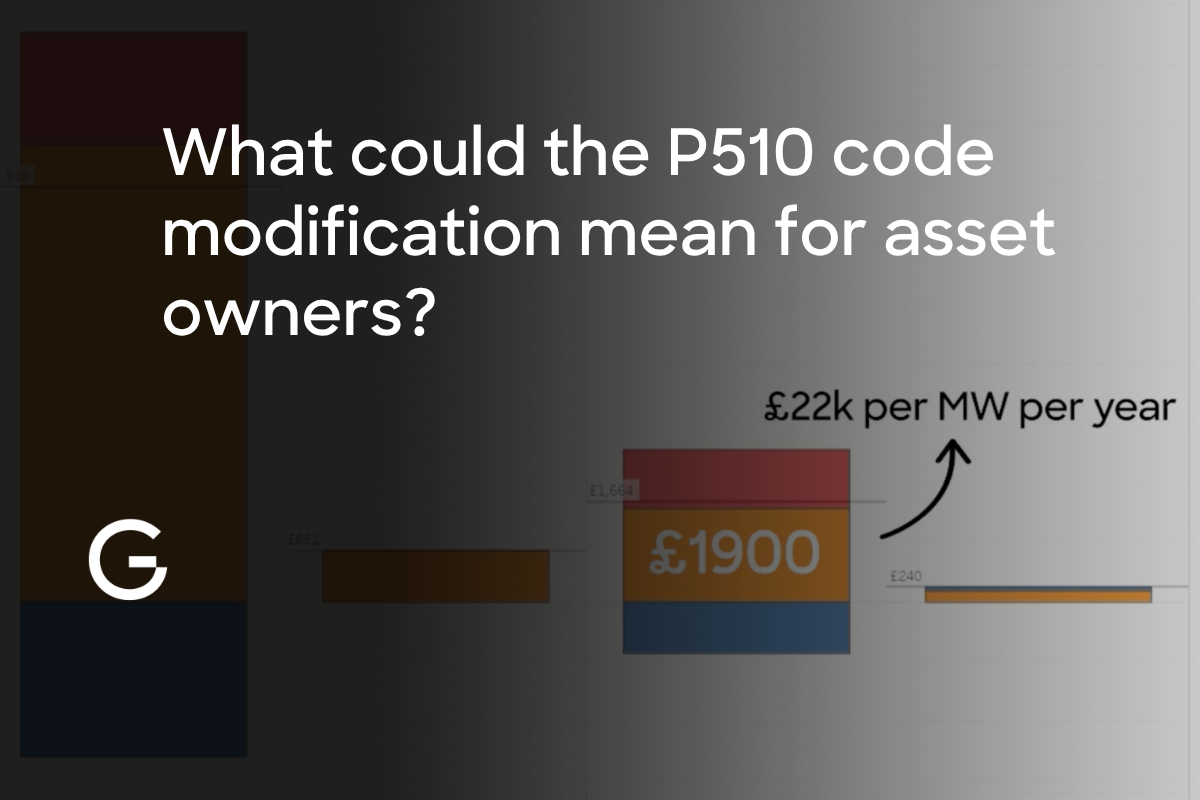

What kind of revenues can asset owners expect under P510?

To explore how P510 could work in practice, we built a model in Gridcog using our inter-asset flow feature, which allows energy flows between assets to be priced separately.

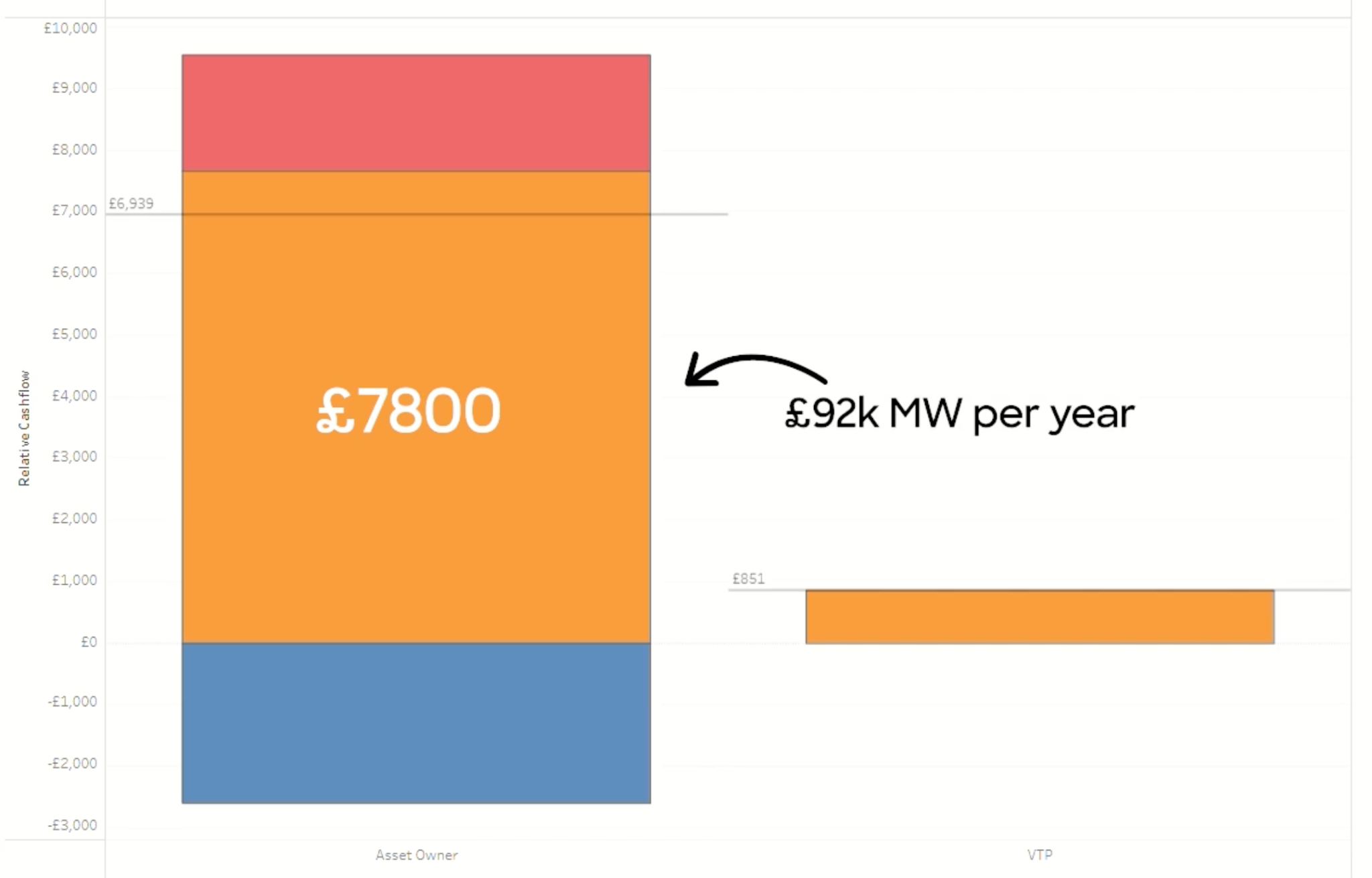

The scenario considers a small industrial site in North Wales with a fixed flat supply contract, analysed across March 2026, with a 1 MW / 2-hour battery optimised for wholesale markets.

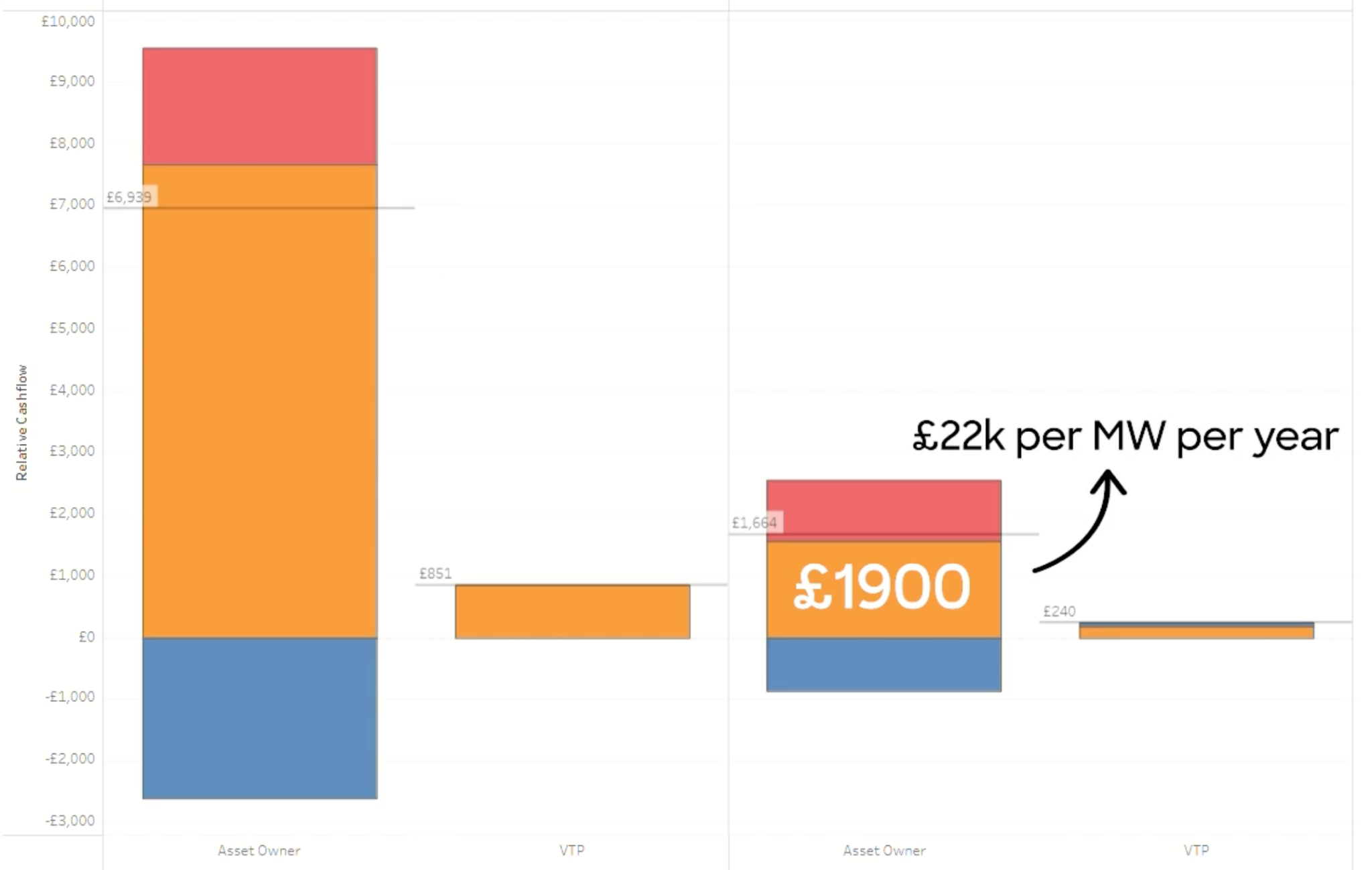

Under P415 (downward deviations only), the battery earns £7,800 over March - equivalent to around £92k per MW per year. This represents the upper bound of value available under the current framework, and highlights a key issue: load-shifting actions can generate disproportionately high revenues that don't reflect genuine system value.

Under P510, the battery earns £1,900 over March - equivalent to around £22k per MW per year. Load shifting is more accurately accounted for, with revenues reflecting a genuine bilateral market signal rather than an artefact of the compensation structure.

What does P510 mean for asset owners and VTPs?

P510 represents a meaningful recalibration of how flexibility is valued in GB. Revenues from load shifting are likely to fall relative to the current P415 arrangement - but they will better reflect real market conditions, and the framework opens up the incentive to shift demand upward as well as down.

For asset owners and VTPs, understanding the implications now - before the modification takes effect - is essential for building robust business cases.

If you'd like to model the implications of P510 for your portfolio, get in touch with the Gridcog team.

.jpg)

.jpg)